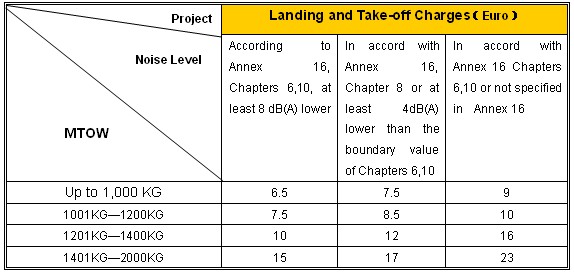

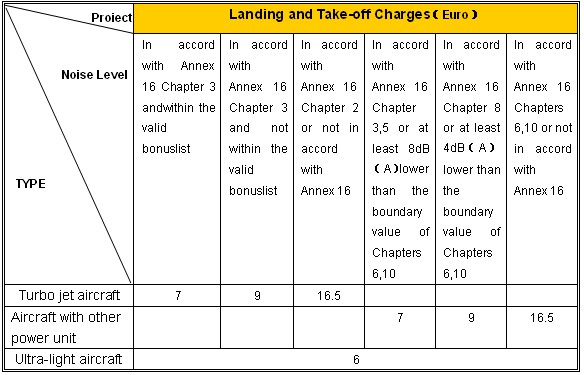

1. Landing and Take-off Charges

Up to 2,000 kg MTOW

More than 2000kg MTOW (per 1000 kg or part thereof)

Discount/ Surcharges :

Training and instruction flights shall be given a discount on landing and take-off charges according to different requirements. Landing and take-off charges are also payable for touch-and-go-landings with immediately ensuing acceleration and take-off of the aircraft. A training flight is a flight in which a civil student pilot, in the context of his or her training at a licensed tainning centre(flight training school), flies under specific conditions to satisfy the requirements for abtaining a civil pilot’s license or an entitlement with respect to the Regulations for Aviation Personnel (Verordnung über Luftpersonal). A instruction flight is a flight which serves to provide flying and technical instruction for civil pilots..

The landing charges should be increased by 50% for IFR landing of the aircraft in question.

No take-off and landing charges is payable for emergency landings due to technical malfunctions of an aircraft or due to hijacking unless the airport is the originally scheduled destination of the flight. Diversionary landings are not emergency landings.

For each landing of an aircraft a landing and take-off charge has to be paid to the airport operator by aircraft owners. The debtors are the airline, the registered keeper of the aircraft; the natural or legal person using the aircraft without being registered keeper of the aircraft. A landing and take-off charge is calculated according to MTOW and noise category of the aircraft. Unless there is special account, the debtor has to pay turnover tax additionally.

2.Other charges

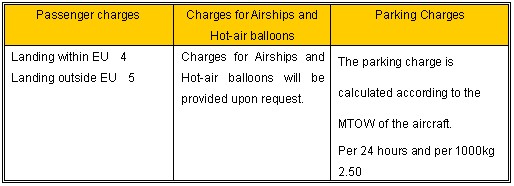

1. Passenger charges: A passenger charge has to be paid to the airport operator by the aircraft keeper when departing. The passenger charge is based on the number of passengers aboard the aircraft when departing. The number of passengers aboard the aircraft on take-off does not include children under two years of age not entitled to occupy a seat. Unless there is special account, the debtor has to pay turnover tax additionally.

2. Parking Charges: A rent (parking charge) has to be paid to the airport operator each time an aircraft is parked at the airport. Debtors of the parking charge are as joint debtors: the airline, the registered keeper of the aircraft; the natural or legal person using the aircraft without being registered keeper of the aircraft or owner. No parking charges will be computed for parking within 6 hours from landing to take-off of the aircraft. A rental contract with special conditions can be signed between the aircraft operator and the airport operator prior to the beginning of the parking for uninterrupted parking which is expected to exceed a period of 30 consecutive days. Unless there is special account, the debtor has to pay turnover tax additionally.

Baltic Airport management Co., Ltd.

Hermann Ertl

Parchim 08.20.2009

German Ministry of Transport, Construction and land Development

Musialczyk

Schwerin 08.24.2009